Family debt lowest in 14 years: Global study

The country’s household debt as percentage of gross domestic product (GDP) has been shrinking over the years from its peak in 2005. The household debt means the purchase of residential property and cars. The household debt, which was 5.1 per cent of the GDP in 2005, fell to 4.1 in 2010. It further decelerated to 3.5 per cent in 2015. The percentage dipped to 3.3 per cent in 2018, lowest in 14 years, according to data prepared by the Institute of International Finance (IIF), a Washington-based organisation. The IIF is the global association of the financial industry, with close to 450 members from 70 countries. According to a study of the Bangladesh Institute of Bank Management (BIBM), more than 80 per cent of the bank finances are concentrated in urban areas. This contraction in percentage is true, but in absolute value this is rising at slow pace compared to the economic expansion.

Source: http://today.thefinancialexpress.com.bd/first-page/family-debt-lowest-in-14-years-global-study-1538239091

Savings tools once again trump bank products

Savers have started to flock back to savings instruments with net sales hitting a six-month high in July as bank deposit products continue to yield underwhelming returns. Net sales of savings instruments stood at Tk 5,036 crore in July, the highest since February, according to the latest data of the Directorate of National Savings Certificates. In January, net investment in the tools stood at Tk 5,140 crore, after which it ranged between Tk 3,100 crore and Tk 4,200 crore. Some banks, however, have set the interest rate as high as 8 percent on their fixed deposit schemes, going back on their promise because of an acute liquidity crunch. In contrast, the interest rate on savings certificates ranges from 11.04 percent to 11.76 percent. The Bangladesh Association of Banks (BAB), a forum of bank directors, had taken a decision to lower the interest rate on savings and lending to 6 percent and 9 percent respectively from July 1, which lured savers to park their funds with government tools. In 2017-18, the government borrowed only Tk 5,666 crore from the banking sector by way of treasury bills and bonds against the annual target of Tk 28,203 crore. The rate of interest on bank borrowings is between 3.10 percent and 8.09 percent. On the other hand, the net sales of savings certificates stood at Tk 46,758 crore last fiscal year against the annual target of Tk 44,000 crore.

Source: https://www.thedailystar.net/business/banking/news/savings-tools-once-again-trump-bank-products-1637815

Spreading agent banking throughout the country

Agent banking is the form of banking that includes limited scale of banking and financial service through persons or agents under a valid agency agreement across the country, especially in remote areas. An agent is a third-party owner of an outlet who conducts banking transactions, such as cash deposit, cash withdrawal, account opening, account inquiries, small-amount loan disbursement, loan recovery, fund transfer, and paying bills under the government safety net programmes on behalf of a bank. Agent banking became popular at the very beginning of operation of the business. The services of agent banks were welcomed by the people, particularly by those who earlier were unbanked. The number of accounts increased to 12,14,367 with deposits of about Tk 13.99 billion (1399.39 crore) at the end of December 2017. At the end of June 2018, the agent banking deposit stood at about Tk 20.12 billion (2012.77 crore) while the number of accounts increased to 17,77,400. There are more than 87,000 villages in the country and the total number of bank branches of all 57 banks are 10,000, most of which are located at district and upazila level. Agent banking should be spread to all the villages. About 86 per cent of total market share of agent banking is held by two banks, namely Bank Asia Limited and Dutch Bangla Bank Limited. If all the banks participated in agent banking proactively, banking system as such would have spread to grassroots people throughout the country. Bangladesh Bank should formulate specific policies in this regard.

Source: http://today.thefinancialexpress.com.bd/views-reviews/spreading-agent-banking-throughout-the-country-1538234108

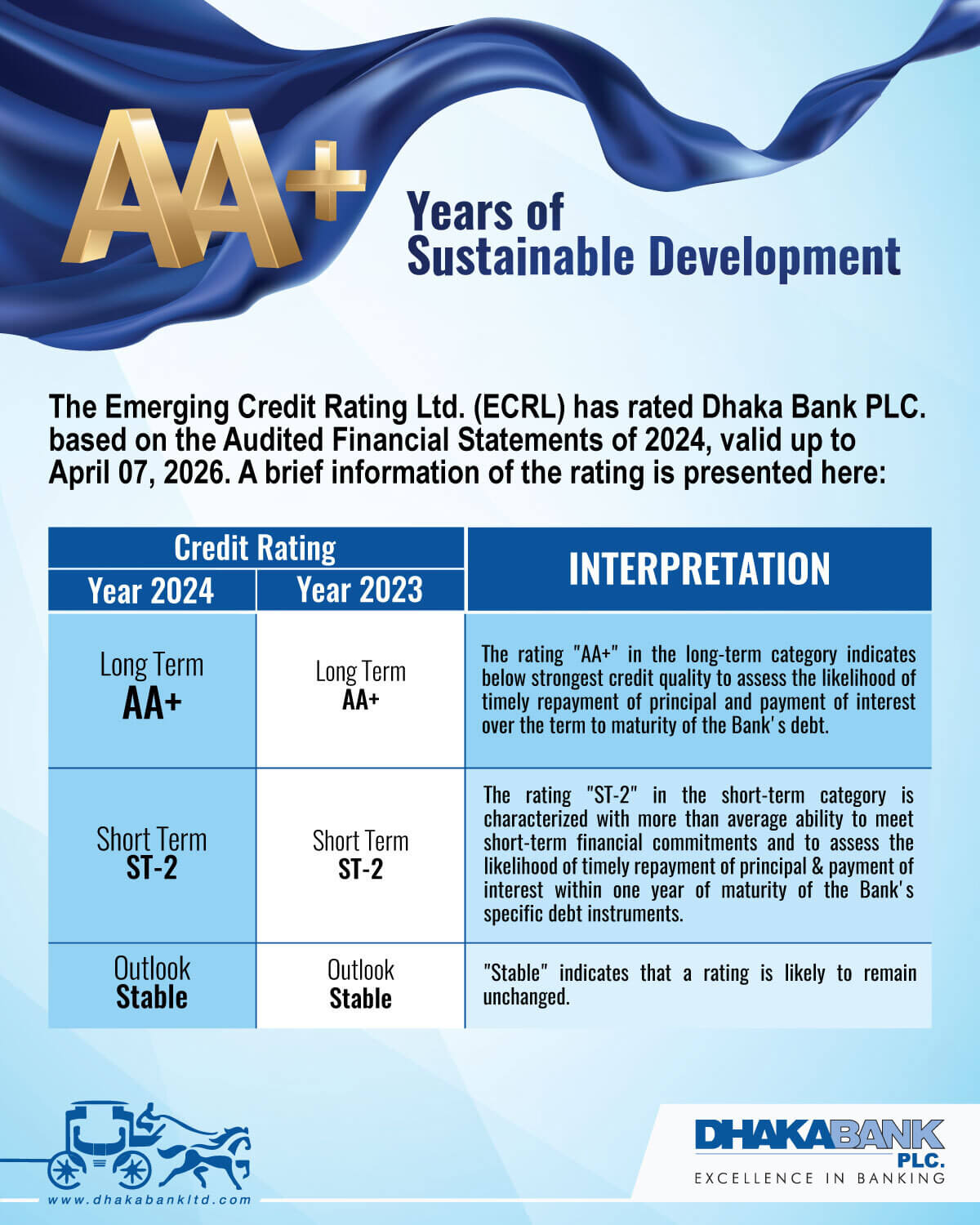

Dhaka Bank launches contactless cards

Dhaka Bank Ltd. has launched a full range of contactless cards with embedded EMV Chip technology with Visa. With this, the bank has embarked on the journey of bringing latest technology of card-based payments in the country. The bank brings Visa signature, platinum and gold credit cards which would bring more speed, convenience and security in everyday payments.

Source: http://today.thefinancialexpress.com.bd/stock-corporate/dhaka-bank-launches-contactless-cards-1538234887

CSE holds investors’ awareness programme

The Chittagong Stock Exchange (CSE) organised a seminar on investors’ awareness, financial literacy and internet trading recently in Cumilla, as part of its plan to ‘promote’ capital market. The seminar was to enlighten investors’ knowledge about the capital market and enhance their expertise in digital trading.

Source: http://today.thefinancialexpress.com.bd/stock-corporate/dhaka-bank-launches-contactless-cards-1538234887

Plant opens in Savar to make pharma equipment

Swiss Biohygienic Equipment (SBE), a joint venture among Bioengineering Switzerland, AMS Technology Germany and Incepta Pharmaceuticals Bangladesh, yesterday opened a plant in Savar to produce hygienic process systems for the pharmaceuticals sector. The 33,000-square feet electro polishing plant will manufacture instruments that are needed to produce pharmaceuticals, Mosaddeque Mahmud Rizwan, managing director of SBE. The plant will also produce pressure vessel, manufacturing vessel and storage vessel for the pharma sector, according to the SBE officials. These vessels are made up of stainless steel to process sterile and non-sterile liquids for the pharmaceuticals sector.

Source: https://www.thedailystar.net/business/news/plant-opens-savar-make-pharma-equipment-1640572

Flying on one engine, global growth exposed to turbulence

With growth in many European, Asian and emerging markets mostly uninspiring, the United States is increasingly the main motor behind the global economy. The world’s biggest economy is under scrutiny, however, as its current upturn is running on borrowed time coming the fiscal stimulus of debt-financed tax cuts. When the downturn in the US economy starts, the effects (on share prices, interest rates, capital flows, emerging countries, exchange rates, global trade and global growth) will be very pronounced. This fiscally induced expansion will be difficult to sustain in the absence of a much more substantial jump in investment to lift the economy’s growth potential. Wages will be in focus with another strong month-on-month rise likely. We probably won’t get a break above 3 per cent year-on-year growth this month, but we certainly expect it next month. Italy’s EU partners will have to figure out quickly whether to come out hard against the decision of Rome’s populist-led government to flout its previous EU fiscal commitments.

Source: http://today.thefinancialexpress.com.bd/views-reviews/developing-skilled-workforce-for-energy-and-power-sector-1538234027

Local and Global Stock Indices *

| Index Name | Close Value | Value Change | Percentage Change |

|---|

| DSEX | 5390.85074 | ↓49.73 | ↓0.11% |

| DJIA | 26,458.31 | ↑18.38 | ↑0.07% |

| FTSE100 | 7,510.20 | ↓35.24 | ↓0.47% |

| Nikkei 225 | 24,120.04 | ↑323.30 | ↑1.36% |

World Commodities *

| Commodity | Close Value | Value Change | Percentage Change |

|---|

| Crude Oil (WTI) | $ 73.25 | ↑1.13 | ↑1.57% |

| Crude Oil (Brent) | $ 82.73 | ↑1.35 | ↑1.66% |

| Gold Spot | $1,190.88 | ↑8.05 | ↑0.68% |

Major Currencies Exchange Rates Movement in Last Seven Days *

| Exchange Rates |

|---|

| USD 1 | BDT 83.9685 |

| GBP 1 | BDT 109.4194 |

| EUR 1 | BDT 97.4370 |

| INR 1 | BDT 1.1583 |

*CURRENCIES AND COMMODITIES ARE TAKEN FROM BLOOMBERG.

{kind=link}